Bookkeeping is the backbone of financial management for any business, and it’s particularly critical for small businesses in the UAE. The unique business environment in the UAE, coupled with specific VAT regulations, makes effective bookkeeping essential for SMEs, freelancers, and other business entities. In this blog post, we’ll walk you through the essentials of managing your books efficiently, ensuring your business prospers.

Understanding Bookkeeping

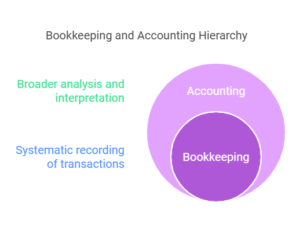

Before diving into the specifics, let’s simplify what bookkeeping involves. Bookkeeping is the systematic recording, organizing, and tracking of financial transactions. It’s an important part of accounting, but while accounting encompasses the broader analysis and interpretation of financial data, bookkeeping focuses on the thorough documentation of daily transactions.

Bookkeeping Basics for Small Businesses in UAE

Setting Up a Bookkeeping System

The first step in effective bookkeeping is establishing a structured system. This involves:

- Choosing the Right Software: Opt for bookkeeping software tailored for small businesses in the UAE. Popular options include QuickBooks, Xero, and Zoho Books. These platforms offer features that comply with UAE’s VAT regulations.

- Chart of Accounts: Create a chart of accounts that categorizes all your business transactions into relevant headings, such as assets, liabilities, income, and expenses.

- Regular Updating: Ensure that financial records are updated daily to avoid backlogs and inaccuracies.

Understanding VAT and Tax Regulations in UAE

VAT regulations in the UAE can be complex, making it essential to keep accurate records. Key points include:

- VAT Registration: Ensure your business is registered for VAT if your annual turnover exceeds AED 375,000.

- Invoice Management: Keep a complete record of all invoices and receipts, as these are crucial for VAT reporting.

- VAT Returns: Submit accurate VAT returns on time to avoid penalties. Use software that automatically calculates VAT to simplify the process.

Key Bookkeeping Practices

Daily, Weekly, and Monthly Tasks

Maintaining a regular schedule for bookkeeping tasks ensures consistency and accuracy.

- Daily Tasks: Record all transactions, update receipts, and monitor cash flow.

- Weekly Tasks: Reconcile bank statements, review expenses, and update accounts payable and receivable.

- Monthly Tasks: Generate financial statements, review the overall financial health of your business, and ensure all records are up-to-date.

Managing Income and Expenses

Accurately tracking income and expenses is essential for a clear financial overview.

- Income Tracking: Record all sources of income, categorize them appropriately, and ensure they align with invoices.

- Expense Tracking: Document all expenses, keep receipts, and categorize them to monitor spending habits.

Reconciling Bank Statements

Regular bank reconciliations help identify discrepancies and ensure your records match your bank statements. This process involves:

- Comparing Transactions: Match each transaction in your bookkeeping records to your bank statement.

- Identifying Errors: Look for and correct any errors or discrepancies, such as missed entries or duplicates.

Tracking Accounts Receivable and Payable

Efficiently managing accounts receivable and payable is critical for cash flow management.

- Accounts Receivable: Monitor outstanding invoices, follow up on overdue payments, and record all incoming payments.

- Accounts Payable: Track due dates for bills, ensure timely payments to avoid late fees, and maintain a record of all outgoing payments.

Common Bookkeeping Mistakes to Avoid

Avoiding the following common bookkeeping mistakes can save you from financial headaches.

- Mixing Personal and Business Finances: Keep separate accounts for personal and business finances to maintain clear records.

- Failing to Keep Receipts and Invoices: Always keep physical or digital copies of all financial documents for reference and audits.

- Not Reconciling Bank Statements Regularly: Regular reconciliation prevents errors and keeps your records accurate.

- Misunderstanding VAT Regulations: Stay informed about VAT rules and ensure compliance to avoid penalties.

Benefits of Hiring Professional Bookkeepers

While Do-It-Yourself (DIY) bookkeeping can be cost-effective, there are significant benefits to hiring professional bookkeepers.

- Expertise: Professional bookkeepers have in-depth knowledge of UAE’s financial regulations, ensuring your books are compliant and accurate.

- Time-Saving: Outsourcing bookkeeping frees up your time to focus on core business activities.

- Error Reduction: Professionals are less likely to make errors, reducing the risk of financial discrepancies.

DIY Bookkeeping Tips and Tools

For those who prefer to manage their own books, here are some valuable tips and tools:

- Use Reliable Software: Invest in reputable bookkeeping software that offers features tailored to small businesses in the UAE.

- Stay Organized: Keep all financial documents well-organized and easily accessible.

- Regular Training: Invest time in learning about bookkeeping practices and stay updated with UAE’s financial regulations.

Frequently Asked Questions (FAQs)

- What is bookkeeping and why is it important?

Bookkeeping involves the systematic recording of financial transactions. It’s crucial for tracking business performance, ensuring tax compliance, and making informed financial decisions.

- What are the key bookkeeping tasks small businesses should focus on?

Key tasks include recording transactions, reconciling bank statements, managing income and expenses, and maintaining accurate records for VAT reporting.

- How do VAT regulations impact bookkeeping in the UAE?

VAT regulations require businesses to keep detailed records of all financial transactions, including invoices and receipts, and submit accurate VAT returns.

- What software is best for bookkeeping for small businesses in the UAE?

Popular options include QuickBooks, Xero, and Zoho Books, all of which offer features that comply with UAE’s VAT regulations.

- Should I outsource my bookkeeping or do it myself?

Outsourcing can save time and reduce errors, but DIY bookkeeping can be cost-effective if you have the knowledge and resources to manage it.

- What are the common bookkeeping mistakes to avoid?

Common mistakes include mixing personal and business finances, failing to keep receipts, not reconciling bank statements regularly, and misunderstanding VAT regulations.

- How can I choose a reliable bookkeeping service in the UAE?

Look for services with positive reviews, relevant experience, and a clear understanding of UAE’s financial regulations.

- What are some tips for effective DIY bookkeeping?

Use reliable software, stay organized, and invest time in regular training to stay updated with bookkeeping practices and regulations.

Conclusion

Effective bookkeeping is vital for the success of SMEs, freelancers, and businesses in the UAE. By implementing the practices outlined in this post, you can ensure accurate financial records, compliance with regulations, and ultimately, the growth of your business.

If managing your bookkeeping sounds overwhelming, let the experts at Beyond Numbers help you! We offer comprehensive and tailor-made accounting and taxation services for businesses in the UAE. With our expertise, you can ensure your financial records are accurate, compliant, and up-to-date, allowing you to focus on growing your business.

Contact Beyond Numbers today to learn more about our services and how we can support your business.